Going for a Run with Hoka of Deckers Outdoors

By Jim Krapfel, CFA, CFP

September 3, 2024

Background

I happened upon Deckers Outdoors Corp. (ticker DECK) through my ownership of Nike (ticker NKE). I noticed that over the course of five quarters, spanning from the second quarter of fiscal 2023 to the second quarter of fiscal 2024 (which ended November 2023), Nike’s currency-neutral revenues tanked from a 27% growth rate to a 1% decline. Nike largely blamed its weak results on a promotional sales environment and a volatile macroeconomic backdrop, but some of its competitors were reporting much better results.

It was clear to me that Nike was losing market share, and at an accelerating rate. I sold off the Nike position across client accounts on December 21, 2023, at $112. I further evaluated the competitive landscape, and two brands stood out for their ability to grow shoe sales at high prices and margins – Hoka and On (ticker ONON). Hoka is owned by U.S.-based Deckers Outdoors, while On is a Swiss company. The brands appeared equally impressive to me, with Hoka’s U.S. domicile serving as the tiebreaker.

I pulled the trigger on buying Deckers across client accounts on January 9 at approximately $700. Through some further buying and price appreciation, the stock became the 9th largest aggregate stock position as of August 31, 2024.

Company Introduction

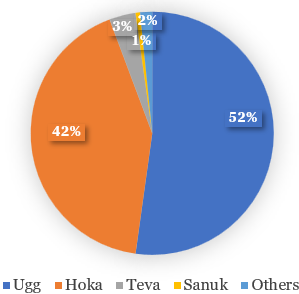

Deckers Outdoors is a collection of five footwear, apparel, and accessory brands – Ugg, Hoka, Teva, Koolaburra, and Ahnu. However, Ugg and Hoka make up over 94% of sales.

Ugg: purchased in 1995, is known for its boots and other footwear that feature sheepskin with a wool inner lining and a tanned outer surface. Its footwear is primarily priced in the $100-$250 range.

Hoka: purchased in 2013 for approximately $1.1 million, is known for its performance footwear that features enhanced cushioning and stability with minimal weight. A pair of Hoka shoes is typically priced in the $125-$190 range.

Teva: modern outdoor lifestyle footwear brand primarily of sports sandals

Koolaburra: value-oriented sheepskin/wool boots complementing Ugg

Ahnu: launched in March 2024, everyday footwear

Figure 1: Revenue by End Market in Fiscal Year 2024 (end March 2024)

Source: Company filings

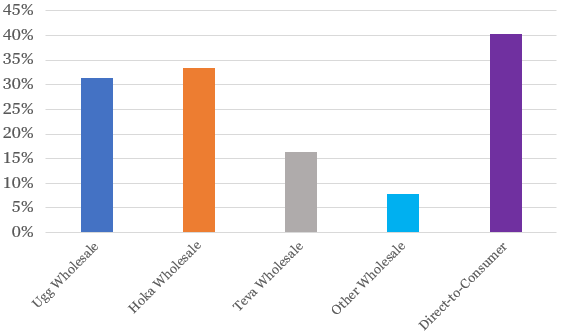

Product sales breakdown by channel in fiscal 2024 was 57% wholesale, such as third-party retailers, and 43% direct-to-consumer, such as through its website in 56 countries, 164 global retail stores (83 concept stores and 81 outlet stores), and 9 flagship stores. As evident below, margins are highest in direct-to-consumer. Product sales breakdown by geography in fiscal 2024 was 67% U.S. and 33% international.

Figure 2: Operating Margins* by Brand and Distribution Channel in FY2024 (end March 2024)

Source: Company filings

*Operating margins are before unallocated overhead costs that were 13% of total revenue

Deckers was founded in 1973 and IPO’d in 1993. At $908/share, it has a market capitalization of $23 billion and is headquartered in Goleta, California. This year has been a busy year for corporate developments, including being added to the S&P 500 on March 18, CEO Dave Powers retiring and being replaced by former Chief Commercial Officer Stefano Caroti on August 1, a sale of the Sanuk brand for an undisclosed amount on August 15, and a 6-for-1 stock split taking place on September 17.

Investment Thesis

We own Deckers Outdoors primarily because of the robust growth outlook for Hoka. It established a reputation for high quality among ultra runners first, which has trickled down to everyday athletes and those who are just looking for a very comfortable shoe. I expect positive word of mouth and enhanced brand recognition to drive further demand for its shoes.

Deckers has carefully managed the growth of Hoka, selectively adding wholesale partners and methodically opening company-owned stores with a longer-term goal of reaching half of sales via direct-to-consumer (versus 38% at Hoka in fiscal 2024). A favorable supply/demand environment for Hoka is evidenced by healthy full-priced selling and Hoka wholesale operating margins of 33% (excluding unallocated corporate costs), compared to 18% at Nike brand, 10% for On, 10% for Skechers (ticker SKX), 4% for Under Armour (ticker UA) and 1% for Adidas (ticker ADDYY). Inclusive of corporate costs and all its brands, Deckers’ operating margins are 22%.

There is ample room for market share gains considering Hoka sales of $1.8 billion in Fiscal 2024 versus Nike footwear sales of $33.4 billion. There also exists some upside potential in expanding into apparel, which is has recently begun. A brand in the early days of reaching the mainstream, expanding distribution and product offerings, and a robust margin profile all point to a long runway of strong growth before Hoka eventually hits a growth wall.

Though not the reason we own Deckers, it is helpful that Ugg sales are resurgent because it still makes up over half of company sales. Ugg reached peak popularity in the 2000s after Oprah Winfrey featured the classic Ugg boot on her famous favorite-things list in 2000, then appetite for the boots became passe by the 2010s. Thereafter, a combination of product innovation and cyclical shifts in fashion boosted Ugg sales, up 16% in fiscal 2024 and up 171% since fiscal 2017. Admittedly, the sustainability of the Ugg brand strength is difficult to judge.

Investors should be rewarded because of the burgeoning amount of free cash flow Deckers is generating. The company repurchased $415 million of stock in fiscal 2024 at an average price of $580/share, helping it reduce its share count by 3%. It bought back another $152 million in the first quarter of fiscal 2025. The stock could get a boost if Deckers announces it is instituting a dividend, which is easily affordable. Deckers has acknowledged it is discussing this with its board of directors.

Although I seek to ride the operating momentum of the business as long as possible, I understand fashion trends can be fickle. If key operating metrics of the business materially worsen, especially at Hoka, I will not hesitate to sell the stock.

Economic Moat

Although Deckers Outdoors has strong brands in Ugg and Hoka, it is a bit of a stretch to say the company has carved out an economic moat, or sustainable competitive advantage. Selling shoes and apparel is highly competitive, fashion trends can reverse on a dime, and none of its brands have become sufficiently established to feel confident saying they will remain strong a decade from now.

That said, with Ugg, and especially Hoka, “brand heat” appears to be strengthening from already high levels, and as such, these brands ought to command premium pricing for the foreseeable future.

Growth, Profitability & Valuation

Deckers Outdoors’ revenue growth should continue to be led by Hoka. Brand sales may struggle to keep pace with the 30%-plus growth rates of the past two quarters, but a growth rate in the 20s should be very achievable over the next several years, absent a recession, as it selectively adds wholesale distribution, retailers give Deckers more shelf space, and especially as it expands in the direct-to-consumer channel. Management’s guidance for 20% revenue growth at Hoka in fiscal 2025 looks very conservative, and I expect this will be raised when it reports fiscal second quarter results in October.

After years of resurgence, it will be challenging to continue growing Ugg sales at a double-digit rate (it grew 14% in the most recent quarter). I expect a steady deceleration to still-healthy growth levels of 10-12% in fiscal 2025 and high-single-digits in fiscal 2026. Here, too, I expect management to increase its fiscal 2025 sales guidance from up mid-single-digits when it reports next quarter given its typical guidance conservatism.

Maintaining margins at these robust levels would be a win. Gross margins reached new highs at both Hoka and Ugg in fiscal 2024, aided by price increases, very strong full-priced selling, and lower freight rates. In recent quarters, management expectations of a normalizing pricing environment has yet to materialize. What is more certain is that freight will turn from a margin tailwind to a headwind as the cost of shipping is on the rise again. Countering the potential pricing and known freight headwinds is an ongoing sales mix shift to the more profitable direct-to-consumer channel. Management has guided for 160-210 basis points (1 basis point is 1/100th of 1%) of operating margin contraction in fiscal 2025, but I expect margins will prove more resilient than that.

All-in, over the next several years I expect mid-teens revenue growth, flat to slightly down operating margins, and mid-teens EPS growth that is aided by growing share repurchases. Given the momentum in the business, I would not be surprised if the company outperforms those expectations.

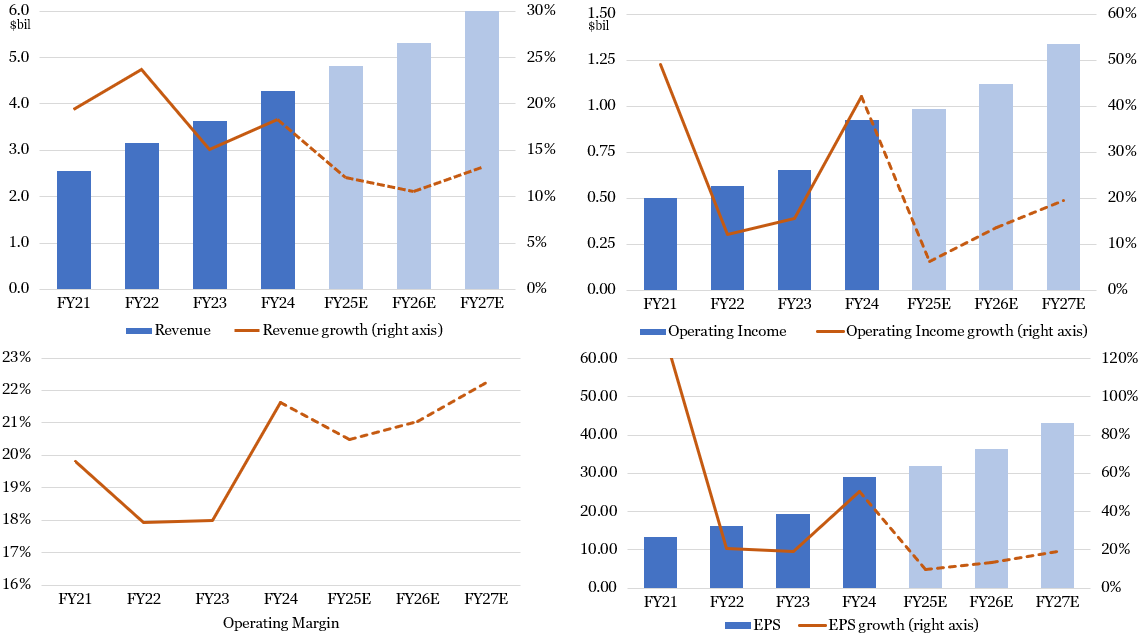

Figure 3: Deckers Outdoors Has a Strong Growth Profile

Sources: Company filings (historical results), Koyfin (analysts’ consensus estimates), Glass Lake Wealth Management

Deckers trades at a reasonable valuation, in my opinion. Its next 12 months’ (NTM) price to earnings (P/E) multiple of 30x exceeds the S&P 500 at 23x NTM, but its growth profile is much stronger than the average company. If Hoka can sustain its strong momentum, then I see room for its valuation multiple to expand.

Key Risks

The biggest idiosyncratic, or company-specific, risks are the health of the Hoka and Ugg brands. There exists a wide range of potential outcomes for both. With Hoka, the biggest risk comes from big competitors like Nike looking to recapture lost market share by launching shoes that mimic Hoka’s trademark cushion and lightweight materials at lower prices. With Ugg, there is more of a fashion risk that its plush boots and footwear go out of style again.

There is also risk that Deckers will make a large acquisition that does not pan out. The risk becomes more acute as it generates more cash and management perhaps becomes overconfident in how it manages brands, but the organic opportunity with its existing brands should keep that risk at bay for a while.

Of course, Deckers is sensitive to changes in consumer spending. If consumers feel less confident about their financial future, then they may look to trade down to less expensive footwear.

Disclaimer

Advisory services are offered by Glass Lake Wealth Management LLC, a Registered Investment Advisor in Illinois and North Carolina. Glass Lake is an investments-oriented boutique that offers a wide spectrum of wealth management advice. Visit glasslakewealth.com for more information.

This blog expresses the views of the author as of the date indicated and such views are subject to change without notice. Glass Lake has no duty or obligation to update the information contained herein. Further, Glass Lake makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, whenever there is the potential for profit there is also the possibility of loss.

This blog is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory, legal, or accounting services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends or market statistics is based on or derived from information provided by independent third-party sources. Glass Lake Wealth Management believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions in which such information is based.