October 2024 Investment Letter

October 1, 2024

First, my heart goes out to those affected by Hurricane Helene’s devastating impacts on the nearby mountain communities of North Carolina and surrounding areas. It is very difficult to hear about the magnitude of destruction. I wish for lives saved and as speedy a recovery as possible.

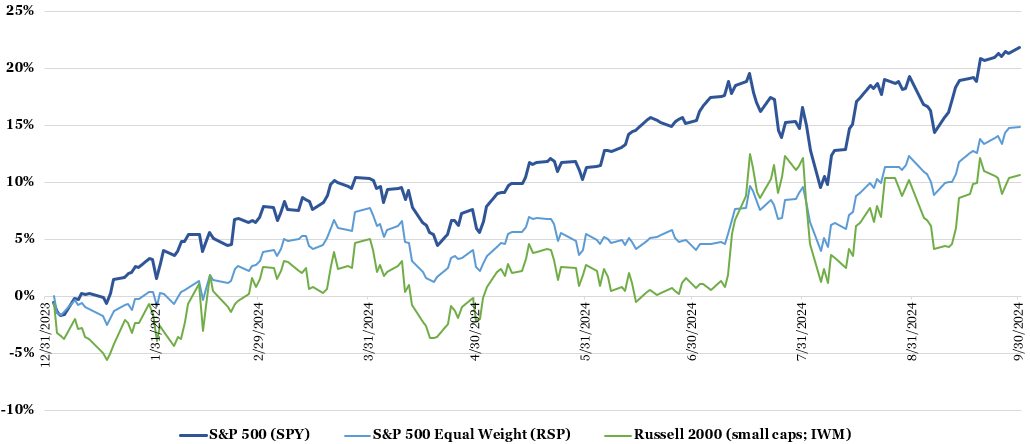

Let us turn our attention to the stock market. In the third quarter, markets continued their ascent. The S&P 500 (SPY), which has a 36% weight in the 10 largest companies, rose 5.8%, bringing its year-to-date return to 21.9%.

The strong performance broadened out from the so-called ‘Magnificent 7’ technology stocks and other megacaps to smaller companies. The equal weighted version of the S&P 500 (RSP) rallied 9.5% in the third quarter, but its 14.9% year-to-date performance still trails its market cap-weighted counterpart. Small caps, as reflected by the iShares Russell 2000 (IWM), appreciated 8.9% in the quarter and 10.6% year-to-date.

Figure 1: Stock Rally Broadens Out Beyond the Mega Caps

Source: Koyfin (inclusive of dividends)

Helping to boost a broader array of stocks is a goldilocks economy -- not too hot nor too cold, and anticipation of a Fed cutting cycle that has just begun. Defying economists’ predictions of a recession a year ago, the consumer continues to spend, albeit unevenly with lower income consumers struggling to pay their bills. Meanwhile, the unemployment rate has creeped up to 4.2% from 3.8% last year, but remains well below the long term average of 5.7%.

Employers having to compete less aggressively for labor, as well as other factors such as normalized supply chains and lower energy prices, has helped to tame inflation to close to the Federal Reserve’s 2% objective (though overall price levels are 19% higher than March 2020).

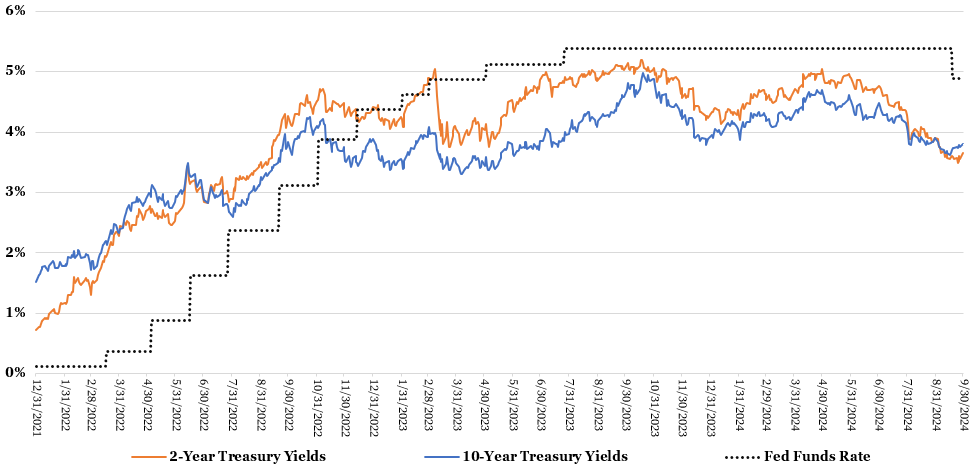

A healthy economy with dramatically slower inflation allowed the Federal Reserve to finally begin cutting rates. On September 18, it made an aggressive move in reducing its Fed Funds rate by 50 basis points (or 0.50%) instead of the more typical 25 basis points adjustment, to 4.75-5.0%. Members of the Fed’s Federal Open Market Committee (FOMC) forecast another 50 basis points of cuts this year, 100 basis points in 2025, and 50 basis points in 2026 (to 2.75-3.0%).

Figure 2: Inflation Has Meaningfully Cooled…

Sources: St. Louis Fed/U.S. Bureau of Economic Analysis. https://fred.stlouisfed.org/series/PCEPI (PCE all-in inflation). https://fred.stlouisfed.org/series/PCEPILFE (PCE core inflation).

Figure 3: …Allowing the Fed to Finally Begin a Rate Cutting Cycle

Sources: St. Louis Fed/Board of Governors of the Federal Reserve System. https://fred.stlouisfed.org/series/DGS2 (2-year US Treasury yield). https://fred.stlouisfed.org/series/DGS10 (10-year US Treasury yield). Forbes Advisor. https://www.forbes.com/advisor/investing/fed-funds-rate-history/ (Fed Funds rate)

The stock market likes lower interest rates, unless it is accompanied by a recession, because bonds become less competitive with stocks, companies can refinance high-interest debt or issue new debt at lower rates, and stocks’ future earnings and cash flows are worth more today using present value calculations. A long-awaited recession does not appear to be forthcoming, so a lower interest rate environment ought to act as a market tailwind, all else equal.

Upcoming Election

Because the presidential election is just five weeks away, it is worth spending some time assessing how potential outcomes could affect the stock market. The most relevant issues to market participants are potential changes in tax policy and their impacts on inflation, budget deficits, and interest rates.

Trump has a highly ambitious tax plan that contains the following major elements. First, his plan lowers the corporate income tax rate to 15% for companies that make their products in the U.S., and to 20% for all others, from 21% currently. Second, he would make the expiring individual income tax cuts from the 2017 Tax Cuts and Jobs Act (TCJA) permanent. Third, he would reinstate an unlimited itemized deduction for state and local taxes (SALT) versus the $10,000 cap at present. Fourth, he would exempt Social Security benefits, tip income, and overtime pay from taxation. Finally, he would seek to help cover the cost of his tax cuts by imposing a universal baseline tariff on all imports of 10-20% and impose a 60% tariff on all imports from China.

Harris has a less specified plan that lays out the following major elements. First, her plan increases the corporate income tax rate to 28%. Second, she would allow the personal income tax provisions from TCJA to expire in 2026. Third, she would increase the top tax rate on long-term capital gains to 28% for taxable income above $1 million and increase the net investment income surtax to 5% (from 3.8%) on income above $400,000. Funds raised through these measures would help fund a tip income exemption, child tax credit expansion, and startup cost deduction increase to $50,000 from $5,000, among other items. There has also been chatter around implementation of a wealth tax and elimination of a step-up in cost basis upon death.

Although many high earners may look favorably upon Trump’s tax plan, the stock market could become concerned by higher resulting inflation and interest rates for the following reasons. First, higher after-tax income for everyone acts as a fiscal stimulus measure that could lead to more inflation, like the effects massive pandemic-era stimulus had on inflation. Second, higher tariffs on imports would surely be passed onto consumers. Third, long-term U.S. Treasury yields could move substantially higher if the rest of the world balks at record budget deficits and government debt. Indeed, analysis from the nonpartisan Penn Wharton Budget Model shows Trump’s economic proposals would increase federal deficits by $5.8 trillion over the next decade, almost five times greater than Harris’ proposals.

Harris’ tax plans, if enacted, would be a clear market negative. Corporations would face a seven-percentage point tax hike, significantly reducing their earnings. Further, higher taxes on long-term capital gains could cause the wealthy to accelerate realized income through sales of appreciated stocks before tax rates rise, hurting stocks. Finally, the prospect of wealth taxes and a step-up of cost basis upon death is especially frightening for the wealthy, but the wealth tax would be nearly impossible to implement and both measures would likely face legal challenges on their constitutionality.

If no new tax legislation is passed, then provisions of Trump’s Tax Cut and Job Act will sunset at the beginning of 2026. The average U.S. taxpayer would see a 2.4% tax increase, with those in high income tax states seeing a smaller increase and those in low income tax states a greater increase because SALT deductions would be back in play.

I see the best-case scenario for the stock market to be a split government that basically ensures neither party’s tax policies become enacted. A split government could be in the form of a Harris presidency with a House and/or Senate controlled by Republicans, or a Trump presidency with at least one chamber of Congress controlled by Democrats. As suggested, the worst-case market scenario is a Democrat sweep, but I would put that probability at under 10% because the Senate appears likely to flip to majority Republican and House control is close to a toss-up.

Client Positioning

I take a long-term view that focuses on compounding returns in a tax-efficient manner. I allocate the bulk of my clients’ equity exposure to “quality growth” companies that possess durable competitive advantages, above-average long-term growth prospects, high levels of profitability and free cash flows, and prudent levels of debt. I generally take a “pruning the weeds and nurturing the flowers” approach of selling stocks that violate my investment thesis and retaining stocks of companies with solid fundamentals. I believe this investment philosophy affords my clients the best shot of generating maximum after-tax, risk-adjusted returns compounded over the long run.

There was not a lot of portfolio activity in the third quarter. Our holdings’ earnings results and outlooks were generally strong over the period, so there was not much pruning to do. Funds coming into portfolios were disproportionally allocated to our most recent new purchases – Eaton (ETN), Vertiv (VRT), and Deckers Outdoors (DECK). I took advantage of pullbacks in shares of Eaton and Vertiv, while I continue to be enthused by the prospects for Deckers and their Hoka shoes, which I wrote up last month.

Nvidia (NVDA) is the company I, as well as many market pundits, pay attention to the most. Its chips continue to have insatiable demand, but questions abound on their sustainability (given a debate on whether its customers will earn an adequate return on their artificial intelligence investment) have whipsawed the stock over the last several months. I expect the stock, which is our third largest position in aggregate, will make another meaningful move higher as investors anticipate substantial growth from its next-generation Blackwell chip that starts shipping in the December quarter. If that happens, then I will likely look to trim the stock as growth could prove difficult to sustain past 2025.

As always, you can expect me to abstain from stocks in long-term challenged industries, such as banking, traditional energy, airlines, and autos. I will also continue to avoid the most speculative areas of the market such as unprofitable growth companies, small biotechnology stocks, and pump-and-dump meme stocks.

For clients’ fixed income portfolios, I continue to overweight low duration holdings (duration is a measure of a bond price’s sensitivity to changes in interest rates). Although the Fed started their rate cutting cycle and short-term interest rates have declined, one can still earn 3.5%-4.0% yields on ultra-safe U.S. Treasuries with one- to two-year maturities, and higher yields for short-duration corporate bonds and mortgage-backed securities. I seek to avoid exposure to longer dated bonds because their yields do not appear to reflect risks regarding the ballooning federal deficit (bond prices fall as yields increase).

Overall asset allocation is likely to remain near current levels. Previously, I was contemplating a higher allocation towards bonds, but with the recent decline in bond yields, I am content with our current bond mix. Note that other than clients who do not have the ability (i.e. an investment horizon of less than a decade) or willingness to take much risk, typically over 90% of assets are in stocks because of their penchant to generate far greater long-term wealth than bonds.

I hope you and your loved ones have a happy, healthy, and wealthy fall season.

Sincerely,

Jim Krapfel, CFA, CFP

Founder/President

Glass Lake Wealth Management, LLC

glasslakewealth.com

608-347-5558

Disclaimer

Advisory services are offered by Glass Lake Wealth Management LLC, a Registered Investment Advisor in Illinois and North Carolina. Glass Lake is an investments-oriented boutique that offers a wide spectrum of wealth management advice. Visit glasslakewealth.com for more information.

This investment letter expresses the views of the author as of the date indicated and such views are subject to change without notice. Glass Lake has no duty or obligation to update the information contained herein. Further, Glass Lake makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, whenever there is the potential for profit there is also the possibility of loss.

This investment letter is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory, legal, or accounting services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends or market statistics is based on or derived from information provided by independent third-party sources. Glass Lake Wealth Management believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions in which such information is based.