Assessing How Much You Really Need to Retire

By Jim Krapfel, CFA, CFP

November 4, 2024

Many people look forward to retirement, but few have a good sense of how much they will need to safely stop working. According to a recent Northwestern Mutual survey, the average American thinks they need $1.46 million saved to retire, up 15% from 2023’s survey. Among those with at least $1 million in investible assets, that number rises to $3.93 million.

An oft-cited rule of thumb for how much to safely spend in retirement is the “4% rule.” Created in 1994 by a financial planner, the 4% rule says to simply sum all investments, withdraw 4% of that total during the first year of retirement, then increase the annual withdrawal by the rate of inflation. It concludes you should be nearly certain of not running out of money during a 30-year retirement across various historical market conditions.

Instead of applying the 4% rule to a known portfolio to determine a safe spending level, we can apply it to a desired retirement spending amount to determine a safe savings level to retire. For instance, a $100,000 annual spending figure implies that one needs $2.5 million ($100,000/.04) to retire.

However, the 4% rule is overly simplistic and makes faulty assumptions for most folks. In this financial blog, I walk through how your unique financial circumstances, objectives, and risk tolerances may augur for a significantly higher or lower safe withdrawal rate that you can use to obtain a better sense of how much you really need to safely retire.

Factors that Influence Your Retirement Number

Desired retirement spending

Determine how much you are spending now and estimate how that might change upon and through retirement.

Consider that numerous studies have shown that most people have U-shaped retirement spending trajectories. People tend to spend more money upon retirement with more time for things like travel. Then as they get older people tend to spend less and stay home more. Near end of life, spending tends to spike as an estimated 70% of people will need long-term care, which has a typical duration of 1 ½ to two years and cost about $100,000 per year.

Flexibility to cut spending

The 4% rule assumes little willingness or ability to reduce spending if things are not going to plan. For instance, your finances could come off track if you unexpectedly opt to financially support your grown children or aging parents. You might also encounter weak investment returns in your early years of retirement, in what is called a “sequence of returns risk.”

However, many people have discretionary spending they are willing to temporarily reduce, if needed. The greater the flexibility to reduce spending, the higher one can target as a safe withdrawal rate, allowing for an improved lifestyle when times are good.

Years of retirement

The 4% rule assumes a 30-year retirement period, but one’s retirement could be considerably shorter or longer. The longer the retirement period, the more conservative the safe withdrawal rate should be.

In determining how long you need to live off your assets, you can first look to actuarial tables on your life expectancy for your age and gender at your intended retirement date. For instance, a typical 65-year-old man can expect live 17 more years while a 65-year-old woman can expect to live 20 more years. Then, factor in your health, family medical history, and a healthy dose of conservatism should you (hopefully) live longer than expected.

Passive income

The 4% rule assumes the retiree will rely solely on their investment portfolio for income during retirement. However, most people will have at least one passive income source.

Social Security benefits are the most common. They apply to anyone with at least 10 years of working and paying Social Security taxes. The benefits can begin between ages 62 and 70, with better payouts the longer you wait (starting date strategy blog here). Others may additionally benefit from pension or rental income.

Passive income reduces the savings needed to safely retire in a couple of ways. First, it can be deducted from your anticipated spending levels. Second, to the extent your passive income is predictable and reliably growing, you can be less conservative on your safe withdrawal rate.

Anticipated inheritances

The 4% rule does not assume any financial windfalls, such as inheritances. As we approach retirement, many of us will have aging parents with some amount of money that will be bequeathed to us. If your parents or other older family members have shared that you are a stated beneficiary, and amounts to be inherited are reasonably known, then it may be appropriate to account for this.

For example, if you determine you need $3 million to safely retire and expect you will inherit about $1 million within the next five years, then you could factor this into your retirement savings requirement, keeping in mind the inheritance could be smaller or occur later than expected. However, it may not be appropriate to incorporate any inheritance if there is sufficient uncertainty or doing so makes you feel financially uncomfortable.

Portfolio taxes

The 4% rule assumes taxes are just another expense you cover with whatever you withdraw. As such, be sure to include taxes payable in your projected retirement spending. How much taxes to incorporate heavily depends on your composition of assets by account type.

The best-case scenario is you have a high proportion of assets in post-tax retirement accounts like Roth IRAs, Roth 401(k)s, or Health Savings Accounts (HSA). Withdrawal, or distributions, from these accounts have no tax impact.

Assets in taxable brokerage accounts need to be accounted for in several ways. First, interest is taxed at your ordinary income tax rate, which ranges from 10%-37% at present. Second, qualified dividends are taxed at 0%, 15%, or 20%, depending on your taxable income and filing status. Third, when you sell a security you have held for under one year, you pay short-term capital gains tax at your ordinary income tax rate. When you sell a security you have held for at least one year, you pay long-term capital gains tax of 0%, 15%, or 20%. Finally, if your total income is above certain thresholds, you pay an additional 3.8% net investment income tax on all these income sources.

Taking distributions from pre-tax retirement accounts like traditional IRAs or 401(k)s face the biggest tax hit. The entire distribution is taxed at your (higher) ordinary income tax rate. Even if you need not withdraw funds from these accounts to fund your lifestyle, you become subject to required minimum distributions at age 73 if born prior to 1960 and age 75 if born in 1960 or later.

Do not forget to additionally account for taxes on state income, Social Security benefits, and other passive income sources, where applicable.

Portfolio returns

The 4% rule makes important assumptions on your asset allocation and returns that are worth explaining.

First, it assumes a balanced asset allocation of around 60% stocks and 40% bonds. You may opt for a higher stock allocation if you have a greater willingness and ability to take risk or have substantial unrealized gains in your stock portfolio. Alternatively, you may opt for lesser stock exposure if your time horizon is shorter and therefore have less time to recover from any performance setback.

Second, the 4% rule assumes that average long-term U.S. stock and bond market returns will persist, which have historically been around 10% for stocks and 6% for bonds. However, those returns are probably too high to assume going forward.

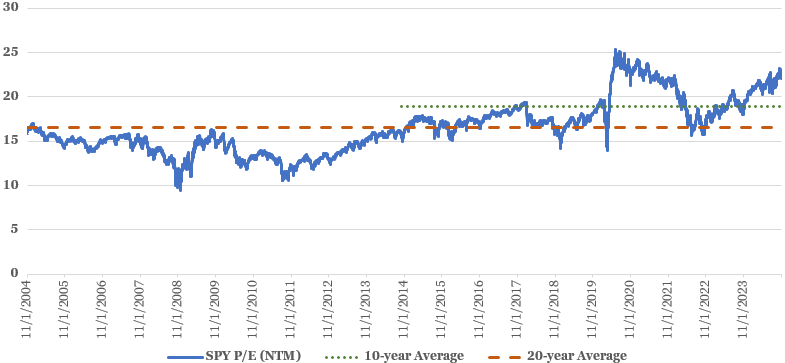

The S&P 500 is trading at 22.1x next-12-months consensus earnings estimates, a 17% premium to the 10-year average and a 33% premium to the 20-year average, according to Koyfin. Corporate profit margins are also near all-time highs, aided by lower tax rates that could be reversed. A more appropriate return assumption for stocks might be 6%-8%.

Figure 1: Stock Valuations are High and Could Suppress Future Returns

Source: Koyfin

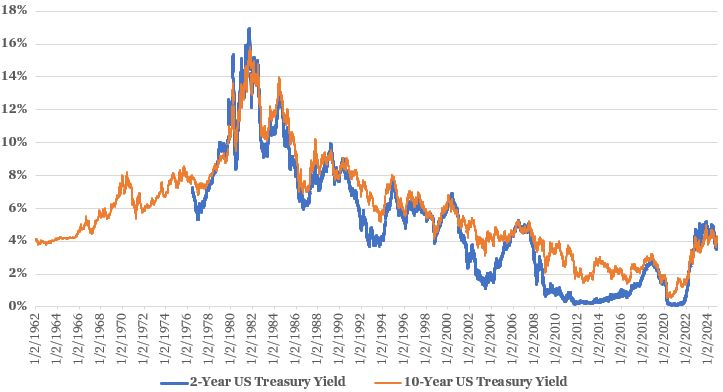

Meanwhile, current interest rates on bonds, while certainly higher than in recent years, are lower than long-term averages. Safe 10-year U.S. Treasury bonds currently yield 4.25%, while corporate bonds, mortgage securities, and other fixed income instruments yield more but carry greater default risk. A more appropriate return assumption for bonds might be 4%-5%.

Figure 2: Bond Yields are Lower than Historical Averages

Sources: St. Louis Fed/Board of Governors of the Federal Reserve System. https://fred.stlouisfed.org/series/DGS2 (2-year US Treasury yield). https://fred.stlouisfed.org/series/DGS10 (10-year US Treasury yield).

Inflation

The 4% rule assumes historical inflation levels of around 3%, above the 2.5% inflation rate I incorporate in my financial planning projections. If inflation runs hotter than expected, then you must increase spending to maintain your lifestyle, which more quickly chips away at your investment portfolio. Persistently high inflation can dramatically increase how much is needed to safely retire.

Legacy intentions

The 4% rule assumes the goal is to simply not to run out of money in your lifetime. However, you may want to ensure you have leftover assets for your children, other loved ones, or charity. If you wish to bequeath a minimum amount to your designated beneficiaries, simply add that to what you need to safely retire without the beneficiaries in mind.

Alternative Safe Withdrawal Rates

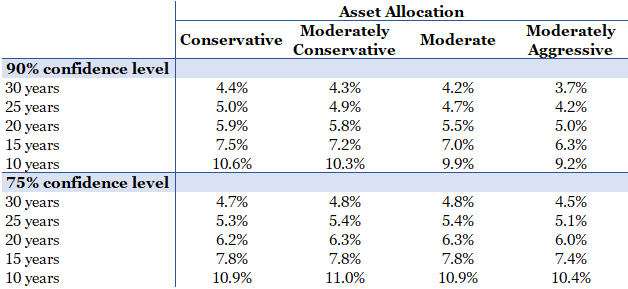

We just established that the 4% rule has serious flaws that render it ineffective for helping you determine your asset level needed to retire. Thankfully, Charles Schwab offers a sound alternative for the safe withdrawal rate, incorporating your (1) time horizon; (2) risk tolerance with respect to your asset allocation; and (3) flexibility to reduce spending, as indicated by the specified confidence levels (i.e. 75% confidence means you have a 75% chance of not running out of money without making spending adjustments). Importantly, it also makes more conservative assumptions for 10-year stock and bond returns.

Figure 3: Schwab’s Suggested Safe Withdrawal Rates

Source: Schwab Center for Financial Research. “Beyond the 4% Rule.” Published May 14, 2024. https://www.schwab.com/learn/story/beyond-4-rule-how-much-can-you-spend-retirement

There are three main takeaways from the table above. The most noteworthy is the inverse relationship between years of retirement and the safe withdrawal rate. The later you retire, the more you can spend before (because of a smaller portfolio needed to retire) and after your retirement date (because of a higher safe withdrawal rate). For instance, reducing your retirement duration from 30 years to 25 years allows for about 12% greater spending per year during retirement, while going from 25 years to 20 years allows for about 17% greater spending.

The second key takeaway is that safe withdrawal rates tend to increase as you position your investments more conservatively. Perhaps counterintuitive, it makes sense because of the greater variance, or volatility, in returns as you allocate more to risky stocks and away from safer fixed income. Keep in mind what you gain in safety you lose in potential wealth generation, so the more conservatively you position your portfolio, the more you sacrifice your potential standard of living and ultimately, the size of your estate.

The third key takeaway is that the less certainty you require to not run out of money, the more you can safely spend in retirement and less assets you need to retire. This touches on your willingness and ability to cut spending in retirement.

Applying Safe Withdrawal Rates to Hypothetical Situations

Schwab’s safe withdrawal table is a good starting point to determine your minimum asset level to retire. Now let us incorporate the other aforementioned factors – passive income, anticipated inheritances, taxes, and legacy intentions – into your retirement equation. I will run through a few hypothetical scenarios to show you how the math works out.

For all scenarios I assume the following:

65-year old with a 30-year time horizon

“Moderate” asset allocation

A good degree of spending flexibility that corresponds to 75% confidence you will not outlive your assets without having to make spending reductions

With these parameters and using Schwab’s table, we can determine that 4.8% is a safe withdrawal rate at your retirement date. For all scenarios, I additionally assume the following:

$100,000 of spending in first year of retirement, before considering taxes

Withdrawals needed to fund spending are proportionate to investment account balances

File taxes as a single person in 2025, standard deduction is taken, and subject to flat 5% state income tax rate

Now, I assume binary “low” and “high” scenarios across passive income, anticipated inheritances, taxes, and legacy intentions:

Passive income scenarios: “low” is $15,000 of Social Security benefits; “high” is $45,000 of Social Security benefits and $30,000 of other taxable passive income

Anticipated inheritances: “low” is none; “high” is $500,000 conservatively estimated within 5 years

Taxes: “low” is portfolio comprised of 50% brokerage, 25% pre-tax IRA, and 25% Roth IRA; “high” is portfolio comprised of 25% brokerage, 75% pre-tax IRA; all positions in brokerage have 100% long-term capital gains with no dividend or interest income

Legacy intentions: “low” is no minimum requirement for beneficiaries to inherit; “high” is minimum requirement of $500,000 for each of two kids plus $200,000 for charities

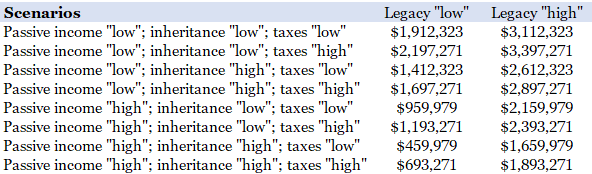

Figure 4: Scenario Analysis on Target Retirement Size using $100,000 of Retirement Spending

Source: Glass Lake Wealth analysis using Schwab’s 4.8% safe withdrawal rate. This table uses hypothetical situations and is provided for illustrative purposes only.

Scenario analysis using just these four factors produces a wide range of portfolios sizes needed to safely retire. This table shows that (1) the greater your Social Security benefits and other passive income, (2) the higher (and sooner) your expected inheritance, (3) the more your investment portfolio is in tax-favored accounts like Roths, and (4) the less importance to leave assets to beneficiaries, the less you need to retire, all else equal. The 4% rule would have suggested $2.5 million is needed given $100,000 of spending, but in many cases, a much smaller portfolio is needed.

Bottom Line

It is critical to go beyond rule of thumb calculations like the 4% rule to help determine how much you need to safely retire. Only by considering your retirement spending, flexibility to cut spending, years of retirement, passive income, anticipated inheritances, portfolio mix, potential portfolio returns, inflation, and legacy intentions will you develop a more realistic sense of your target retirement number.

That is a lot to consider and beyond the scope of analysis for most people. To better comb through the factors involved and your unique situation, consider working with a financial advisor to develop a comprehensive financial plan that will give you the best insight.

Disclaimer

Advisory services are offered by Glass Lake Wealth Management LLC, a Registered Investment Advisor in Illinois and North Carolina. Glass Lake is an investments-oriented boutique that offers a full spectrum of wealth management advice. Visit glasslakewealth.com for more information.

This blog is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory, tax, legal, insurance or accounting services or an offer to sell or solicitation to buy insurance, securities, or related financial instruments in any jurisdiction. Certain information contained herein is based on or derived from information provided by independent third-party sources. Glass Lake Wealth Management believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions in which such information is based.