Manufactured Home Stocks Produce Profits

By Jim Krapfel, CFA, CFP

December 2, 2024

Introduction

Instead of focusing on a single stock, I will be highlighting three companies we own that all reside in the manufactured home (MH) industry: Champion Homes (ticker SKY; formerly known as Skyline Champion), Cavco Industries (ticker CVCO), and Legacy Housing (ticker LEGH). I will share my bullish long-term thesis for the MH industry and explain why we own each company.

Background

I first came across the MH industry during my days as a homebuilding stock analyst at research firm Morningstar (ticker MORN) from 2011 to 2015. I took my bullish long-term overall housing outlook – informed by years of housing underproduction and favorable demographic trends – to wealth management firm RMB Capital. There, I conducted deep-drive research on the MH industry and met senior members of Champion’s and Cavco’s management teams at investor events and their manufacturing plants.

I made my first personal MH stock purchase when I bought Cavco in May 2015. I started buying Champion in August 2017 and it has been among my largest personal holdings since early 2018. I initiated a position in Legacy in February 2021 that I continue to hold.

I have consistently purchased Champion for client accounts since my firm’s founding in April 2020. I started buying Legacy for clients in July 2021 at around $17/share and Cavco in August 2021 at about $240/share. Champion was the 5th largest aggregate stock position across client accounts as of November 30, and Cavco and Legacy were smaller positions. On average, the three stocks make up about 10% of clients’ individual stock allocations.

Industry Overview

The MH industry is distinct from traditional site builders. Whereas homebuilders like D.R. Horton (ticker DHI), Lennar (ticker LEN), and Pulte (ticker PHM) build homes directly on lots, the MH industry constructs homes in a manufacturing plant, in one or more sections, then transports homes via truck to the home site where finally assembly and utility hookups take place.

Price is a distinguishing factor for the MH industry. The average sales price of a MH is about $122,000, a small fraction of an existing home of about $501,000 and a new site-built home of about $546,000. Manufactured homes are typically much smaller, but on a per square foot basis, MH is still much cheaper, at about $131/sq ft vs. $226/sq ft for an existing home. Notably, the cost of manufactured homes do not include land, so that cost needs to be factored in, whether purchased separately or rented. Fifty-nine percent of new MH are placed in a MH community, where average monthly rents are about $650.

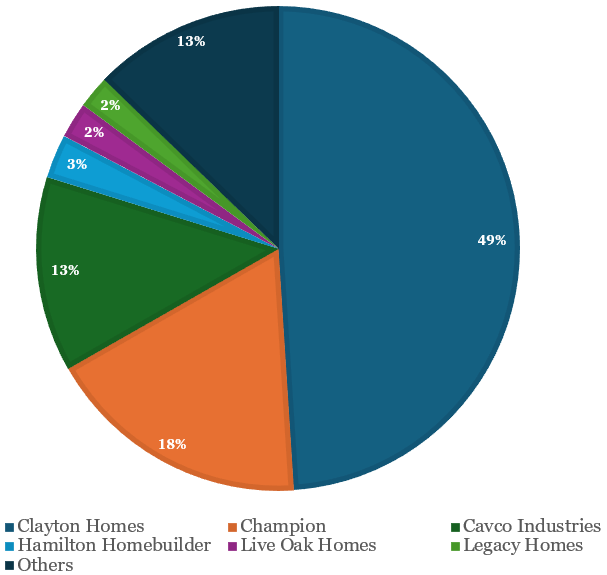

Three companies account for 80% of MH shipments. Clayton, owned by conglomerate Berkshire Hathaway (ticker BRKB), makes up about half of the industry. Champion, Cavco, and Legacy are the only pure-play publicly traded MH companies.

Figure 1: Manufactured Home Market Share by 2023 Shipments

Source: MH Insider. “Manufactured Housing Industry Trends & Statistics.” Accessed 11/27/24. https://mhinsider.com/manufactured-housing-industry-trends-statistics/

Although Champion, Cavco, and Legacy all operate in the MH industry, there are a couple notable distinctions. First, Cavco uniquely owns a subsidiary that provides property and casualty insurance to owners of MH. Over the last four years, this business has ranged from 3% to 19% of Cavco’s pre-tax profit, and its profitability is highly dependent on the occurrence of severe weather events like wind and hail.

Second, Legacy uniquely has an established financing operation in which it provides consumer loans directly to MH buyers and inventory financing to MH dealers and community operators. Its lending business typically makes up about half its profits. In contrast, Champion and Cavco mostly partner with third party lenders and do not take on material default risk.

Present-day Champion was formed via the larger, highly profitable, privately held Champion Enterprise Holdings merging with the smaller, struggling, publicly traded Skyline in June 2018. Cavco became a publicly traded company in 2003 when it was spun off from its parent company, Centex, a traditional homebuilder. Legacy Housing went public in December 2018 via an initial public offering that priced at $12/share. The market capitalizations of the three companies are approximately $6 billion, $4 billion, and $600 million, respectively.

Investment Thesis

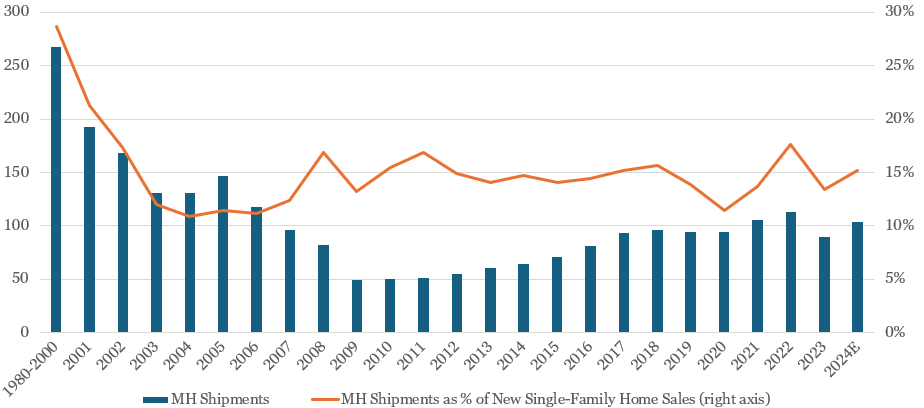

The biggest component to my long-running, long-term bullish thesis on the MH industry is that it addresses the housing affordability crisis. Consumer housing affordability issues have become even more pronounced of late as the average 30-year fixed mortgage rate spiked from sub-3% to nearly 7% over the last three years and house prices shot up an additional 20% over the same time period. That results in a ~90% higher mortgage payment! I expect manufactured homes’ strengthening value proposition to allow the industry to regain market share from site-built homes and give MH industry participants greater latitude to increase their own pricing.

Figure 2: Manufactured Home Industry Has More Room to Recover

Sources: U.S. Census Bureau https://fred.stlouisfed.org/series/SHTNSAUS (MH shipments), https://fred.stlouisfed.org/series/HSN1FA (annual new single family, site-built homes sold), https://fred.stlouisfed.org/series/HSN1FNSA (monthly new single family, site-built homes sold)

A second big industry tailwind is improved consumer financing. Financial institutions exited the MH loan market from 1999 through 2002 as consumer default rates soared and prices of the relatively poorly-constructed homes of the 1990s soured. MH buyers either had to pay cash or rely on financing from the several remaining lenders that charged chattel (chattel is home-only, not the land) rates around five-percentage points higher than conventional loans. Since then, several MH lenders have entered the market, with chattel spreads over conventional loans having narrowed to 1.5%-2.0%.

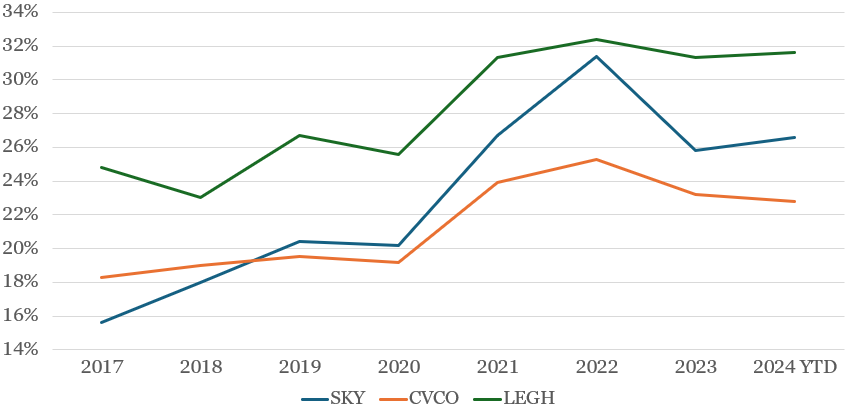

A third big industry tailwind is that it has evolved into what I call a rational oligopoly. The competitive intensity among industry participants has lessened over the years as smaller players either failed (especially during the housing bust of 2008-2012) or were acquired by the big three companies. This shows up in Champion’s, Cavco’s, and Legacy Housing’s gross margins that have strongly trended up over time, only pulling back when MH volumes decline. I expect the long-term margin trend to continue its ascension as the number of competitors in any given market retrench further through acquisitions.

Figure 3: Manufactured Home Segment Gross Margins Have Materially Improved

Source: Company filings

Notes: (1) SKY and CVCO have fiscal years that end in March, so I have adjusted their results accordingly (i.e. Fiscal 2024 results are shown as 2023). (2) LEGH has higher gross margins primarily due to its focus of selling through company-owned retail locations (sales to independent retail locations, communities, and builder developers carry lower gross margins).

In addition to these longer-term industry drivers, there are a few cyclical tailwinds that ought to boost the industry over the next year or two. First, now that interest rates are trending flat to down, MH consumers’ sticker shock should fade, and pent-up demand ought to be released. Second, the community sales channel (30-40% of industry sales) should continue its recovery as these customers fully return to typical ordering following a ~12 month destocking period. Third, I expect substantial orders from FEMA in the quarters ahead because of the need to rebuild housing stock following highly destructive hurricanes Helene and Milton. Deliveries to FEMA typically carry favorable margins too.

Champion is our largest MH stock position because I consider it to be best-of-breed in the industry. It has been the most focused on organic growth, has made the most impressive inroads with the growing builder developer sales channel, and has executed best on delivering strong margins. Further, Champion’s recent equity investment in ECN, owner of Triad Financial Services, allows it to establish a captive financing operation, which could facilitate greater market share gains without incurring default risk.

Cavco is a bit more conservative than Champion, dedicating more of its available cash to buying back stock at what has proven to be favorable prices. Share buybacks have been large enough to reduce its year-over-year share count by about 5%, boosting earnings per share, without it having to take on any debt. I see Cavco as having somewhat less upside share price potential than Champion, but more downside protection.

Legacy is a bit of a different animal with its major lending operations. You can think of it as part MH company, part highly profitable community bank. Book value is as important a valuation reference point as its earnings per share, and its book value per share has compounded at a 14% rate since its 2018 IPO, to $19.84/share at the end of September. Not fully reflected in its book value is the 1,025 acres of owned Texas land, purchased from April 2018 to February 2021, that should monetize over the next few years.

Economic Moat

Although these companies have many positive attributes, they are among the few client holdings that I do not believe possess an economic moat, or sustainable competitive advantage. The MH industry has limited points of differentiation to the consumer and it does not take a lot of time, nor capital, to get a new MH plant permitted and built.

However, accessing sufficient labor is often a key constraint to boosting output. There is also a certain amount of manufacturing best practices that can take years to perfect. So, although strong economic returns may not sustain over the very long run (10+ years from now), I expect a multi-year period in which industry participants can achieve outsized profits.

Growth, Profitability & Valuation

Consensus estimates for MH companies’ sales, margins, and earnings are understated, in my view. The cyclical tailwinds are robust, and I don’t think the Street is incorporating much, if any, FEMA revenue because orders were not yet received as of their latest earnings reports (but the companies indicated “substantial” orders are forthcoming).

Recovering industry volumes, ultimately exceeding the 2023 cyclical peak, should materially boost industry gross and operating margins as well. Once industry capacity utilization crosses ~80% (vs. likely 60%-70% now), companies gain significant pricing power, as they wielded in 2021 and 2022.

Over the next two years, EPS growth rates for Champion and Cavco ought to exceed 20%, perhaps much higher if the economy stays strong and interest rates cooperate. Over a five-year period, I think EPS ought to expand at a double-digit pace driven by high single-digit revenue growth, higher margins, and a lower share count, especially at Cavco. Legacy is likely to experience slower but more consistent revenue and EPS growth, with book value per share growth in the low- to mid-teens.

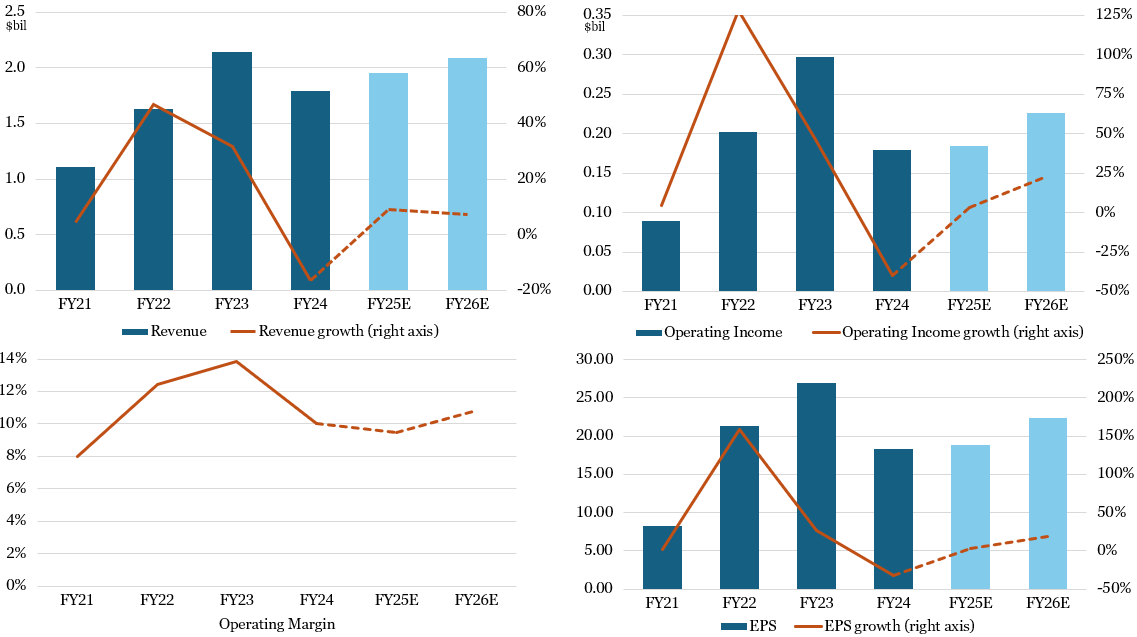

Figure 4: Consensus Estimates on Champion’s Revenue and Profitability

Sources: Company filings (historical results), Koyfin (analysts’ consensus estimates), Glass Lake Wealth Management

Figure 5: Consensus Estimates on Cavco’s Revenue and Profitability

Sources: Company filings (historical results), Koyfin (analysts’ consensus estimates), Glass Lake Wealth Management

Figure 6: Consensus Estimates on Legacy’s Revenue and Profitability

Sources: Company filings (historical results), Koyfin (analysts’ consensus estimates), Glass Lake Wealth Management

Champion’s and Cavco’s next 12 months’ (NTM) price to earnings (P/E) multiples of 28.8x and 24.6x, respectively, appear reasonable in my view. In comparison, the S&P 500 trades at 23.0x NTM. The companies’ better short- and long-term growth outlooks are partially offset by their high cyclicality, smaller size, and lack of sustainable competitive advantages. Meanwhile, Legacy trades with a 10.7x NTM P/E multiple and a 1.3x book value multiple, attractive levels for a company with more modest growth but strong return metrics.

Key Risks

The biggest risks for all three companies are a weak economy and rising interest rates. When lower income consumers are not gainfully employed, they will not feel comfortable enough to buy any home, even if it is much cheaper than a traditional site-built home. Also, their consumers tend to balk in periods of rising interest rates as affordability can become challenged. The MH industry is highly cyclical, as evidenced by the 66% peak-to-trough decline in shipments during the housing crash (2005-2009), and to a lesser extent, the 21% decline in 2023 in response to rising interest rates.

Key idiosyncratic, or company-specific, risk factors include execution on Champion’s and Cavco’s future acquisitions since that is a material component to each companies’ growth plans. Cavco faces additional risks in its property and casualty insurance arm as profitability can greatly fluctuate year to year. Legacy faces additional risks from (1) its lending customers becoming financially impaired and possibly defaulting; and (2) it two founders, who appear to be stepping away from day-to-day operations, more quickly sell off the ~54% of Legacy shares they and their family members own.

Disclaimer

Advisory services are offered by Glass Lake Wealth Management LLC, a Registered Investment Advisor in Illinois and North Carolina. Glass Lake is an investments-oriented boutique that offers a wide spectrum of wealth management advice. Visit glasslakewealth.com for more information.

This blog expresses the views of the author as of the date indicated and such views are subject to change without notice. Glass Lake has no duty or obligation to update the information contained herein. Further, Glass Lake makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, whenever there is the potential for profit there is also the possibility of loss.

This blog is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory, legal, or accounting services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends or market statistics is based on or derived from information provided by independent third-party sources. Glass Lake Wealth Management believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions in which such information is based.