January 2025 Investment Letter

January 2, 2025

The fourth quarter added onto what was already a banner year for the stock market. The S&P 500 (SPY) rose 2.8% over the past three months, bringing its full year total return (inclusive of dividends) to 26.4%. This follows a nearly identical 26.2% total return in 2023.

The market rally was largely confined to the very largest companies, especially technology-oriented, in the fourth quarter and full year. As displayed below, the 20 largest companies in the S&P 500 averaged a 9% gain for the quarter and 48% for the year. By contrast, the other 479 companies in the index averaged a 2% loss and 14% gain, respectively. The iShares Russell 2000 (IWM), an ETF holding small cap stocks, lagged as well, with gains of just 1% and 13%.

Figure 1: Stock Rally Still Fueled by the Mega Caps (owned stocks bolded)

Sources: Koyfin (inclusive of dividends), Glass Lake Wealth Management

Fortunately, we held a fair share of the megacaps that performed so well in 2024. We held four of the so-called ‘Magnificent 7’ stocks – Nvidia (NVDA), Microsoft (MSFT), Alphabet (GOOG), Amazon (AMZN) – and seven of the largest 20 companies by market capitalization in our approximately 25 stock portfolios.

Looking at what drove fourth quarter market performance, the November election figured prominently. The market cheered Republicans sweeping the presidency, House of Representatives, and Senate because Republican control holds the prospect of lower taxes and lighter regulation. More specifically, lawmakers will likely extend or make the individual income tax cuts from the 2017 Tax Cuts and Jobs Act (TCJA) permanent and could further reduce the corporate tax rate from the current 21%. Installation of new regulators – from the SEC, FTC, DOJ, and beyond – ought to ease capital requirements for banks, open the floodgates for crypto investing, make it easier for large companies to make acquisitions, and lower regulatory burdens for many businesses.

The market initially ignored potential downsides of the incoming administration. Key economic risks include the effects of proposed tariffs – 10% to 20% on all imports to the U.S., a 60% or more tariff on goods from China, and a threatened 25% tariff on goods from Canada and Mexico -- on inflation. If large deportations of illegal immigrants are delivered as promised, then there could be labor shortages in certain parts of the economy, which could act as another inflation stimulant. Finally, the budget deficit could balloon further if tax rates decline, potentially stoking U.S. Treasury yields higher.

The Federal Reserve recently took notice of the upside inflationary risks despite narrowly deciding to cut the fed funds rate by another 25 basis points on December 18. During the accompanying press conference, Fed Chairman Jerome Powell signaled that any further cuts are on hold until inflation makes more meaningful downward progress. Members of the Federal Open Market Committee (FOMC) still forecast 50 basis points of cuts in 2025, down from 100 basis points of cuts forecasted three months prior, but the bias appears to be for fewer cuts.

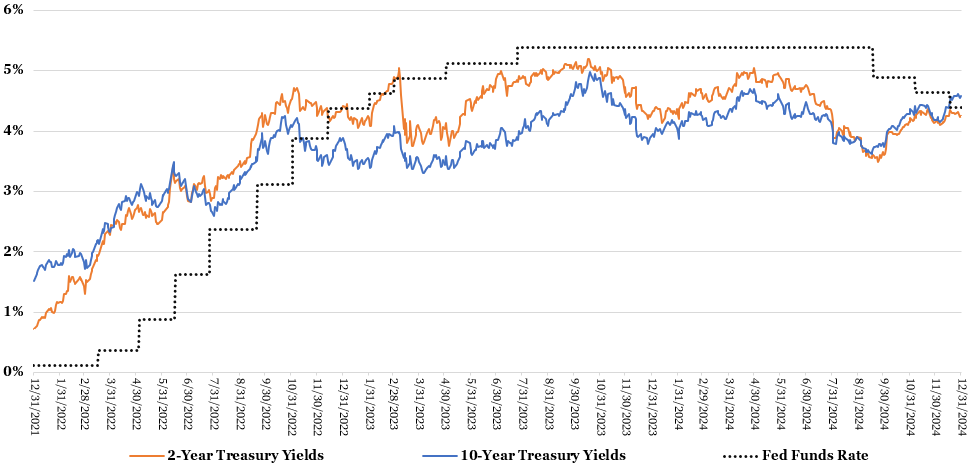

The influential 10-year Treasury bond responded in kind, with its yield bouncing back near its cycle highs. Higher yields took some of the excitement out of the stock market over the final two weeks of the year as higher bond yields better compete for investors’ dollars, companies face higher financing costs, and stocks’ future earnings are worth less today.

Figure 2: 10-Year Treasury Yields Back Near Cycle Highs

Sources: St. Louis Fed/Board of Governors of the Federal Reserve System. https://fred.stlouisfed.org/series/DGS2 (2-year US Treasury yield). https://fred.stlouisfed.org/series/DGS10 (10-year US Treasury yield). Forbes Advisor. https://www.forbes.com/advisor/investing/fed-funds-rate-history/ (Fed Funds rate)

Market Outlook

Past results may not be indicative of future results, but I thought it would be interesting to see how the S&P 500 performed after consecutive 20%-plus years. According to Yahoo Finance, it has happened only four times before, mostly recently in 1998 (marking a third consecutive 20% year). In each occurrence, the S&P 500 rose the following year, by an average of 20%. Given the very small sample size, I would give these results little credence to how 2025 might perform.

Rather, I expect the stock market will be driven by policy, especially tariffs, and their effects on economic growth, inflation, and interest rates. If the Trump administration negotiates deals with other countries such that implemented tariffs are much smaller than threatened, then the inflation impact ought to be contained. If tariffs are implemented in full, then I could envision a meaningfully negative market reaction. However, Trump then might decide to reverse course given his fixation on the stock market as a yardstick of job performance.

Overall, I believe strong momentum in the U.S. economy, pro-economic policies likely to be implemented, and increasing productivity benefits from artificial intelligence (AI) will outweigh negatives such as potential tariffs and significant deportation, and high stock market valuations. I would be surprised to see another 20%-plus market performance in 2025 though.

As I have often implored, it is a fool’s errand to act on any prediction of the economy and overall stock market performance. There are countless interrelated factors that are nearly impossible to predict with enduring accuracy. Instead, I strive to tune out the noise, stay true to an asset allocation that makes sense given one’s return objectives, risk tolerance, and time horizon, and stick to individual company fundamentals.

Client Positioning

I take a long-term view that focuses on compounding returns in a tax-efficient manner. I allocate the bulk of my clients’ equity exposure to “quality growth” companies that possess durable competitive advantages, above-average long-term growth prospects, high levels of profitability and free cash flows, and prudent levels of debt. I generally take a “pruning the weeds and nurturing the flowers” approach of selling stocks that violate my investment thesis and retaining stocks of companies with solid fundamentals. I believe this investment philosophy affords my clients the best shot of generating maximum after-tax, risk-adjusted returns compounded over the long run.

Portfolio activity was high in the fourth quarter after a quiet third quarter. The most consequential change was the purchase of Bitcoin through the Grayscale Bitcoin Mini Trust (BTC) for clients that did not object to the purchase of this attractive but risky investment. I purchased Bitcoin a few days after the U.S. presidential election for reasons described in the table below. Amounts purchased were subject to clients’ varying risk tolerance levels and were contained to 1% to 4% of client assets. Bitcoin, often referred to as “digital gold,” was funded through partial sales of a gold ETF (IAU) and complete sale of a silver ETF (SIVR).

The other notable change was a swap of Advanced Micro Devices (AMD) for Marvell Technology (MRVL). I first trimmed AMD last January for Nvidia (NVDA), then again in October for more Alphabet (GOOG) shares, and decided to sell the remainder in December to fund a small purchase of Marvel. Marvell’s robust third quarter results, along with its new 5-year agreement with Amazon’s AWS cloud computing unit, convinced me that it will benefit from AI’s generational opportunity more so than AMD. I will be looking to add to our Marvel position if the stock is weak to start the year.

Meanwhile, I still patiently wait for the opportunity to trim our large weighting in Nvidia (NVDA), a company I worry will have difficulty sustaining high growth rates beyond this year. However, I am not willing to do so below $150/share at present. Most of my clients’ Nvidia holdings are in taxable accounts in which shares were purchased in early January of last year, so any sale going forward will ensure taxes will be paid at the more favorable long-term capital gains rate (when held for at least one year).

Figure 3: Portfolio Changes in Majority of Client Accounts in 4Q 2024

Source: Glass Lake Wealth Management

As always, you can expect me to abstain from stocks in long-term challenged industries, such as banking, traditional energy, airlines, and autos. I will also continue to avoid the most speculative areas of the market such as unprofitable growth companies, small biotechnology stocks, and pump-and-dump meme stocks.

For clients’ fixed income portfolios, I continue to overweight low duration holdings (duration is a measure of a bond price’s sensitivity to changes in interest rates). As mentioned earlier, the Republican sweep portends a deepening of deficit spending. This could put pressure on the yield curve, meaning medium and longer-term Treasury yields (with maturities of five years and later) could significantly rise (and their bond prices fall).

Overall asset allocation is likely to remain near current levels. However, if the stock market continues to show strong performance, thereby increasing the likelihood of an eventual painful correction, then I may trim our exposure to stocks in favor of short-dated bonds. Note that other than clients who do not have the ability (i.e. an investment horizon of less than a decade) or willingness to take much risk, typically over 90% of assets are in stocks because of their penchant to generate far greater long-term wealth than bonds.

I hope you and your loved ones had an enjoyable holiday season. I wish you a happy, healthy, and wealthy start to the new year!

Sincerely,

Jim Krapfel, CFA, CFP

Founder/President

Glass Lake Wealth Management, LLC

glasslakewealth.com

608-347-5558

Disclaimer

Advisory services are offered by Glass Lake Wealth Management LLC, a Registered Investment Advisor in Illinois and North Carolina. Glass Lake is an investments-oriented boutique that offers a wide spectrum of wealth management advice. Visit glasslakewealth.com for more information.

This investment letter expresses the views of the author as of the date indicated and such views are subject to change without notice. Glass Lake has no duty or obligation to update the information contained herein. Further, Glass Lake makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, whenever there is the potential for profit there is also the possibility of loss.

This investment letter is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory, legal, or accounting services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends or market statistics is based on or derived from information provided by independent third-party sources. Glass Lake Wealth Management believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions in which such information is based.