Mercado Libre is Driving E-Commerce Growth in Latin America

By Jim Krapfel, CFA, CFP

March 3, 2025

Background

I first came across Mercado Libre (ticker MELI) while researching companies for personal investment some time in 2017 or 2018. I was immediately impressed with its leadership position and growth profile in the underpenetrated e-commerce category in Latin America. As the company successfully scaled its business to reach profitability, I started buying for my personal account.

I have consistently purchased MELI shares for client accounts since my firm’s founding in April 2020. The first client purchase was at $586/share. Mercado Libre was the 8th largest aggregate stock position across client accounts as of February 28.

Company Introduction

Mercado Libre operates an online commerce and fintech ecosystem in Latin America. Its business is divided into two segments – Commerce and Fintech.

In its Commerce segment, Mercado Libre can be considered the Amazon (ticker AMZN) of Latin America. Via its Mercado Libre Marketplace, it sells an assortment of products ranging from consumer electronics, apparel & beauty, home goods, auto accessories, toys, books, entertainment, and consumer product goods. Over 90% of the goods transacted come from third-party sellers. It also facilitates shipment of goods through a mix of company-owned and third-party fulfillment centers and delivery vehicles.

In its Fintech segment, the company can be considered part PayPal (ticker PYPL), part Block (formerly known as Square; ticker XYZ), and part American Express (ticker AXP). This “Mercado Pago” arm operates a suite of solutions that facilitate payments on and off its marketplace, as well as offering digital banking services. It also extends credit to merchants and consumers through credit lines, personal loans, and credit cards.

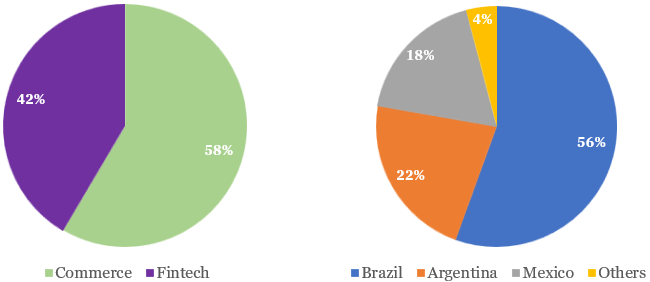

Revenue is concentrated in Brazil, Argentina, and Mexico, but it also operates in 15 other Latin America countries such as Chile, Colombia, Peru, Uruguay, Venezuela, Bolivia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Honduras, Nicaragua, Panama, Paraguay, and El Salvador.

Figure 1: 2024 Revenue by Segment and Country

Source: Company filings

The company is headquartered in Montevideo, Uruguay and is incorporated in Delaware. The company had its initial public offering in 2007 and it sported a market capitalization of $1.3 billion at the end of the first day of trading. The company has ballooned to a $108 billion market cap as of the end of February.

Investment Thesis

A big reason I like Mercado Libre is the secular (long-term) growth opportunity in Latin American e-commerce. According to Mercado Libre management, e-commerce as a percentage of retail sales is only 15% across Latin America, compared to over 25% in the U.S. and more than 40% in China. In Mercado Libre’s biggest markets of Brazil, Argentina, and Mexico, e-commerce sales penetration has reached 9%, 18%, and 15%, respectively. As more sales move online given growing recognition of its convenience and greater breadth of products available to purchase, I expect Mercado Libre’s Commerce segment to be a strong beneficiary.

A secondary reason I like Mercado Libre is that its Fintech segment ought to have outsized growth with a diminishing risk profile over time. The company is rapidly expanding its digital banking operations that should serve to increase monetization of its e-commerce business and grow its fee and interest income from customers outside its retail marketplace who are underserved by traditional banks. Thus far the company has been able to do this by securitizing receivables, allowing it to avoid becoming a traditional bank. Mercado Libre should be able to refine who it wants to lend to as it applies its AI-powered credit risk analysis to a maturing lending data set, driving better credit quality and lower credit losses over time.

Growth in Mercado Libre’s advertising revenue should provide a long-term margin tailwind. The company is still early in its ad penetration across its marketplace, with advertising revenue at 2.1% of its gross merchandise value in its latest quarter, up from 1.6% a year prior. The opportunity for further penetration is big when considering Amazon’s advertising revenue was 10.9% of its global retail sales last quarter. Mercado Libre does not disclose its margins on ad sales, but they are surely greater than the corporate average.

A fourth and final element to my positive thesis on Mercado Libre is a more favorable political environment in the company’s highest margin country of Argentina. Macroeconomic and political uncertainty have been a mainstay in Argentina, but the election of President Javier Milei in 2023 has shifted the country toward more market-friendly policies that has already brought down the country’s monthly inflation rate to 2.2% in January from a recent peak of 25% (and annual inflation peaking at nearly 300% in early 2024). A more stable environment in Argentina should allow Mercado Libre to see continued accelerated growth in the country that started in the second half of 2024.

Economic Moat

I believe Mercado Libre has carved out an economic moat, or sustainable competitive advantage, largely because of its strong network effects and its vast logistics and fulfillment infrastructure. Its economic moat ought to help the company profitably defend against new and existing competitors looking to make inroads.

Network effects are in place when the value of a platform increases as more buyers and sellers participate. With over 100 million active users and millions of merchants, Mercado Libre enjoys a self-reinforcing ecosystem that makes it more difficult for new entrants to compete. More specifically, as the ecosystem grows larger, sellers benefit from quicker inventory turnover and access to a larger pool of potential customers, while buyers benefit from wider product breadth, lower shipping costs, and enhanced search engine optimization.

Its logistics network, called Mercado Envíos, is the other key differentiator. The company has invested considerable resources in its network to provide faster and more reliable delivery than competitors. Indeed, Mercado Envíos handles over 95% of deliveries on its marketplace, and 49% of items are being delivered same-day or next-day, something competitors that mostly rely on countries’ postal services cannot provide. Faster, more reliable deliveries create a better customer experience, ultimately driving greater customer retention rates and purchase frequency.

Growth, Profitability & Valuation

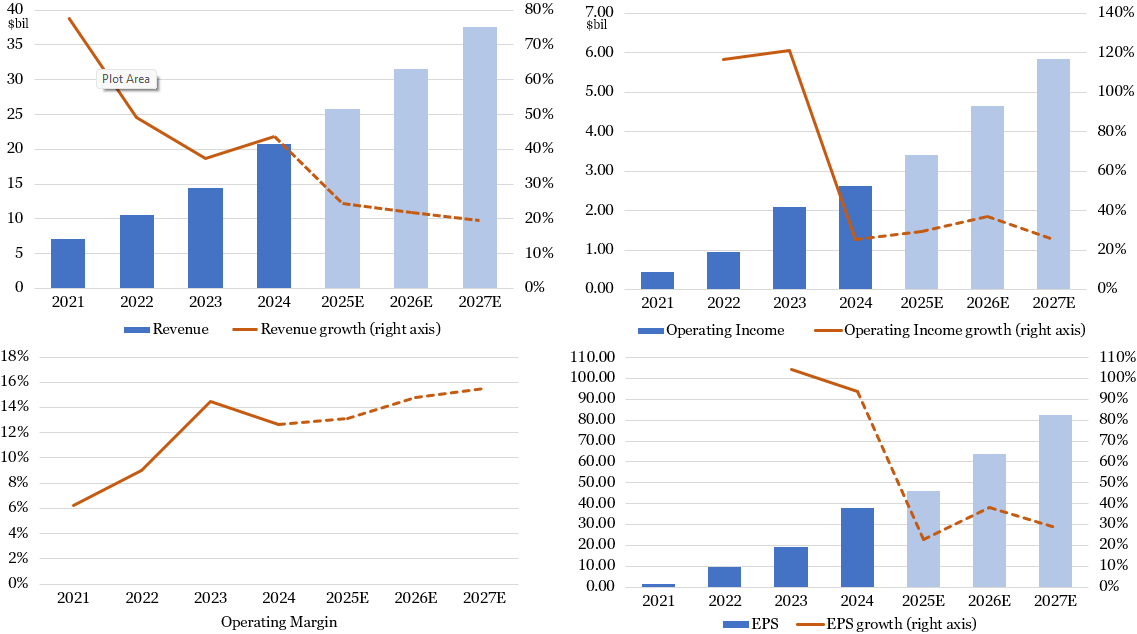

Mercado Libre’s reported foreign exchange-neutral revenue growth, which hovered around 100% throughout 2024, is not the best growth metric because it is heavily influenced by its operating countries’ often high and volatile inflation rates. It is better to look at its revenues denominated in U.S. dollars, which grew 44% in 2024. Analysts’ consensus estimates call for a revenue growth deceleration to the low- to mid-20s, but I expect reported growth to come in considerably better than that given the secular growth opportunity, reacceleration in Argentina, and the company’s history of growing faster than analyst expectations.

The company’s operating margins are artificially constrained by an accounting requirement to recognize anticipated (but not realized) credit losses upfront at time of loan origination while associated revenues are recognized throughout the life of the loan. Because it started to more rapidly expand its credit business in 2024, its streak of rapidly expanding annual margins came to a halt last year, and short-term margins could be similarly constrained. However, underlying margins continue to improve because of the firm’s operating leverage and disciplined cost management. I foresee renewed margin expansion to new highs once the credit business moves beyond this hypergrowth stage.

Flattish margins over the next year or two implies EPS growth about in line with revenue growth, which I expect to be greater than 30% in USD. When margins positively inflect, EPS growth should inflect too.

Figure 2: Mercado Libre is Firmly on a Strong Growth Trajectory

Sources: Company filings (historical results), Koyfin (analysts’ consensus estimates), Glass Lake Wealth Management

Mercado Libre commands a next 12 months’ (NTM) price to earnings (P/E) multiple of 46x, well ahead of the S&P 500’s 24x. I think the premium multiple is well-deserved because of its persistently high growth profile and near-term EPS that is artificially depressed by high growth in its credit portfolio. Adjusting for more normalized growth in credit, Mercado Libre’s NTM P/E is closer to 38x. I expect the stock to gradually move higher and really break out when it signals slower growth in credit (and therefore lower provisions for bad debt).

Key Risks

The biggest idiosyncratic, or company-specific, risk is that the competitive environment worsens, leading to slower revenue growth and lower margins. In Brazil, Mercado Libre faces a strong competitor in Singapore-based Shopee, which has a growing lead for app and URL traffic (Mercado Libre is #2). Mercado Libre also competes with China’s Shein, Temu, and Alibaba, and Amazon in Brazil. Mercado Libre’s competitive positioning is stronger in Mexico but it faces the same set of formidable competitors. The competitive environment has been more benign in Argentina, where Mercado Libre holds a dominant position.

Macroeconomic risks are aplenty for this Latin American company. One or more of its geographies could experience an economic slowdown, political turmoil, currency weakness, regulatory difficulties, or tax changes. Realization of these risks could serve to slow growth, make it more costly to operate, and/or drive higher credit losses. Health of the credit business is of particular importance given its rapid expansion.

Disclaimer

Advisory services are offered by Glass Lake Wealth Management LLC, a Registered Investment Advisor in Illinois and North Carolina. Glass Lake is an investments-oriented boutique that offers a wide spectrum of wealth management advice. Visit glasslakewealth.com for more information.

This blog expresses the views of the author as of the date indicated and such views are subject to change without notice. Glass Lake has no duty or obligation to update the information contained herein. Further, Glass Lake makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, whenever there is the potential for profit there is also the possibility of loss.

This blog is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory, legal, or accounting services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends or market statistics is based on or derived from information provided by independent third-party sources. Glass Lake Wealth Management believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions in which such information is based.